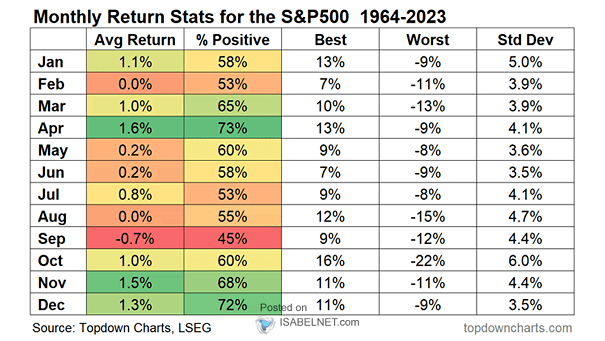

S&P 500 Seasonality

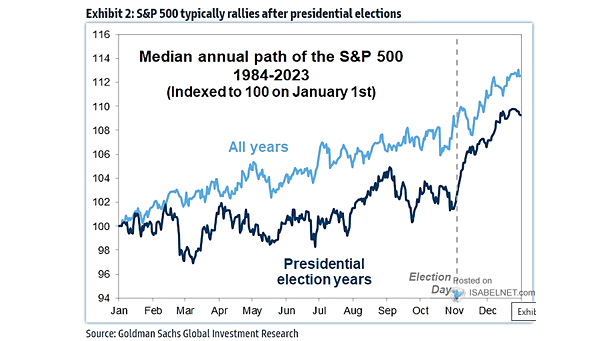

S&P 500 Seasonality From Election Day in November to the end of the year, the S&P 500 index has historically seen a median return of 4%, reflecting a seasonal pattern where investor optimism and holiday spending boost market performance. Image: Goldman Sachs Global Investment Research