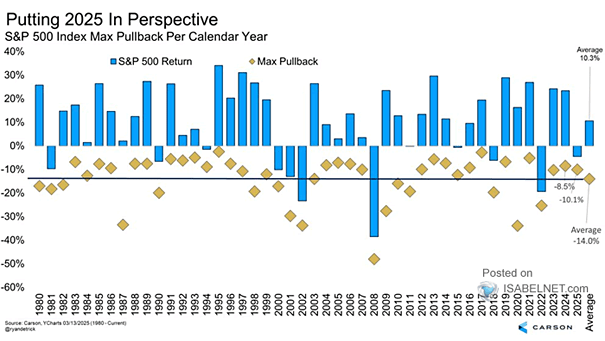

S&P 500 Index Max Pullback per Calendar Year

S&P 500 Index Max Pullback per Calendar Year March’s 9% pullback may already be the year’s deepest. If so, the market has less room for another major selloff. Back-to-back drawdowns of that size are rare,…