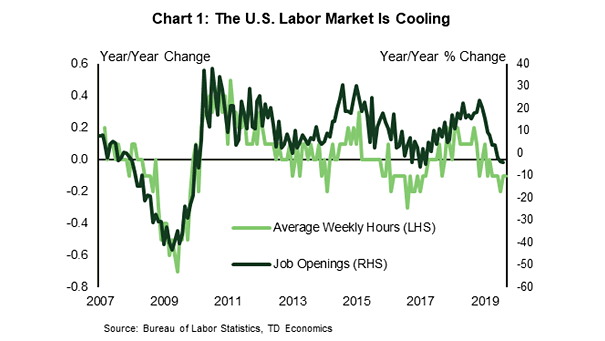

Job Openings and Average Weekly Hours

Job Openings and Average Weekly Hours The number of job openings fell in August, mirroring the decline in average weekly hours, and confirming that the U.S. labor market is cooling. Image: TD Bank Financial Group