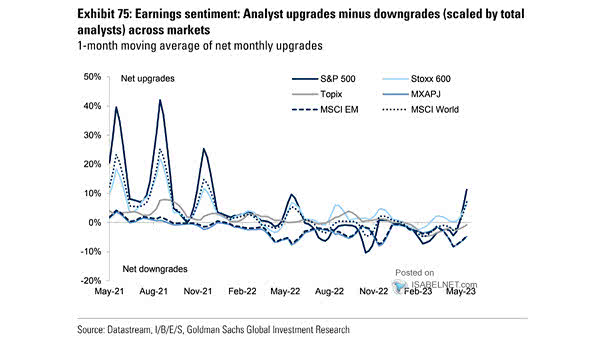

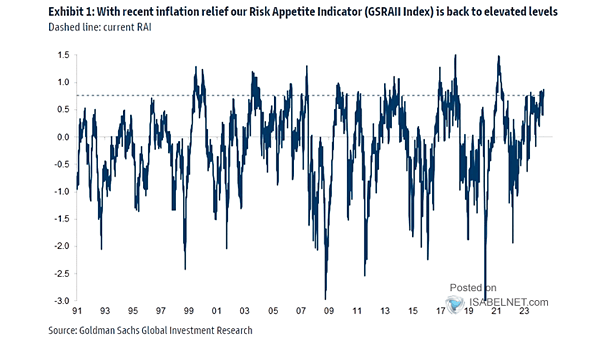

Risk Appetite Indicator Level and Momentum Factors

Risk Appetite Indicator Level and Momentum Factors Goldman Sachs’ Risk Appetite Indicator increased again, keeping markets firmly in risk-on territory. Image: Goldman Sachs Global Investment Research