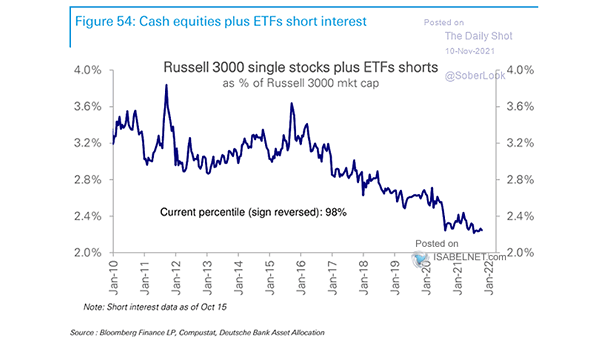

Median Short Interest Across Russell 3000 Stocks

Median Short Interest Across Russell 3000 Stocks Median short interest across Russell 3000 names has surged to multi-year highs as bearish positioning intensifies, setting the stage for a potential squeeze. Crowded shorts have a habit of turning into aggressive buying. Image: Deutsche Bank Asset Allocation