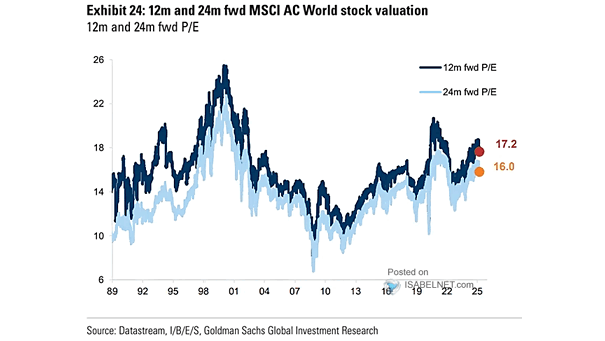

Valuation – MSCI World 12-Month Forward P/E

Valuation – MSCI World 12-Month Forward PE With global equities trading at 18.5 times forward earnings, valuations look stretched by historical standards. Not a bubble, but far from cheap. Image: Goldman Sachs Global Investment Research