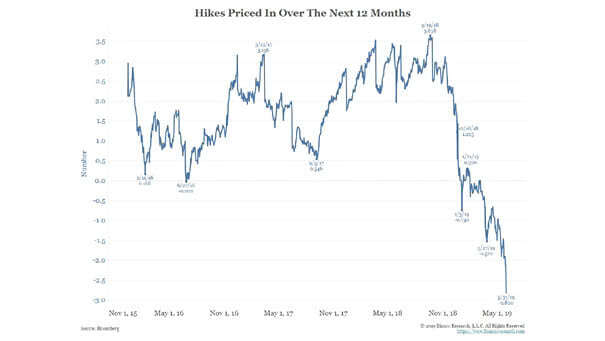

The Fed Fund Futures Market Is Pricing Three Rate Cuts Over the Next 12 Months

The Fed Fund Futures Market Is Pricing Three Rate Cuts Over the Next 12 Months According to CME Group, the Fed fund futures market is pricing three rate cuts over the next 12 months. You may also like “Markets Have Accurately Priced in Cuts before Easing Cycles Begin“ Image: Bianco Research LLC